Autoregressive Moving Average (ARMA): Sunspots data¶

[1]:

%matplotlib inline

[2]:

import matplotlib.pyplot as plt

import numpy as np

import pandas as pd

import statsmodels.api as sm

from scipy import stats

from statsmodels.tsa.arima.model import ARIMA

[3]:

from statsmodels.graphics.api import qqplot

Sunspots Data¶

[4]:

print(sm.datasets.sunspots.NOTE)

::

Number of Observations - 309 (Annual 1700 - 2008)

Number of Variables - 1

Variable name definitions::

SUNACTIVITY - Number of sunspots for each year

The data file contains a 'YEAR' variable that is not returned by load.

[5]:

dta = sm.datasets.sunspots.load_pandas().data

[6]:

dta.index = pd.Index(sm.tsa.datetools.dates_from_range("1700", "2008"))

dta.index.freq = dta.index.inferred_freq

del dta["YEAR"]

[7]:

dta.plot(figsize=(12, 8))

[7]:

<Axes: >

[8]:

fig = plt.figure(figsize=(12, 8))

ax1 = fig.add_subplot(211)

fig = sm.graphics.tsa.plot_acf(dta.values.squeeze(), lags=40, ax=ax1)

ax2 = fig.add_subplot(212)

fig = sm.graphics.tsa.plot_pacf(dta, lags=40, ax=ax2)

[9]:

arma_mod20 = ARIMA(dta, order=(2, 0, 0)).fit()

print(arma_mod20.params)

const 49.746198

ar.L1 1.390633

ar.L2 -0.688573

sigma2 274.727181

dtype: float64

[10]:

arma_mod30 = ARIMA(dta, order=(3, 0, 0)).fit()

[11]:

print(arma_mod20.aic, arma_mod20.bic, arma_mod20.hqic)

2622.6370933008184 2637.570458408409 2628.6074811460644

[12]:

print(arma_mod30.params)

const 49.751912

ar.L1 1.300818

ar.L2 -0.508102

ar.L3 -0.129644

sigma2 270.101140

dtype: float64

[13]:

print(arma_mod30.aic, arma_mod30.bic, arma_mod30.hqic)

2619.4036292456663 2638.070335630155 2626.8666140522237

Does our model obey the theory?

[14]:

sm.stats.durbin_watson(arma_mod30.resid.values)

[14]:

np.float64(1.9564953616090044)

[15]:

fig = plt.figure(figsize=(12, 8))

ax = fig.add_subplot(111)

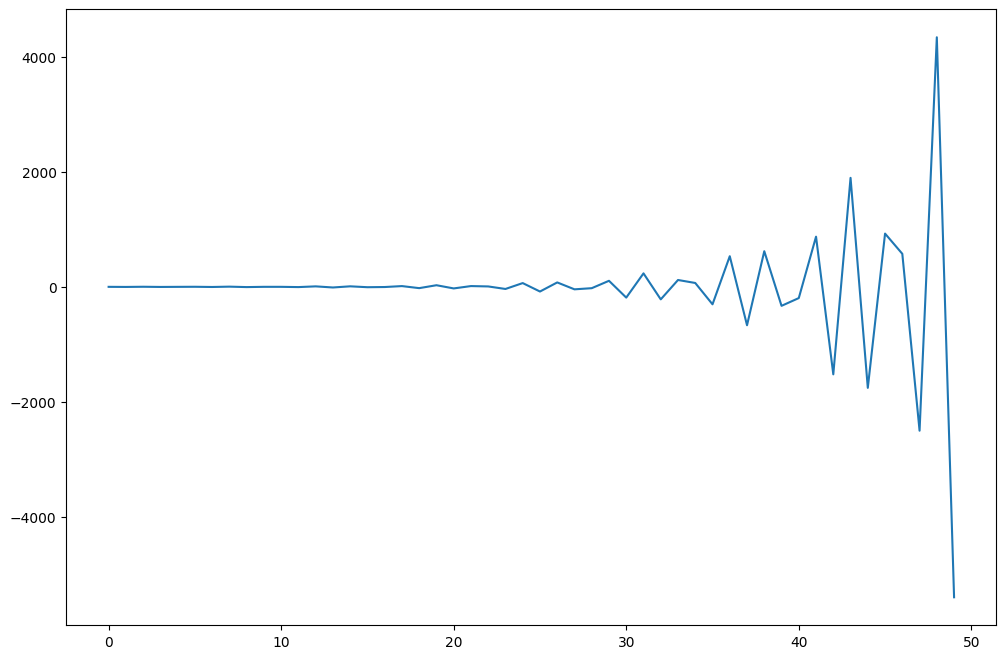

ax = arma_mod30.resid.plot(ax=ax)

[16]:

resid = arma_mod30.resid

[17]:

stats.normaltest(resid)

[17]:

NormaltestResult(statistic=np.float64(49.843932188649774), pvalue=np.float64(1.5015079882540518e-11))

[18]:

fig = plt.figure(figsize=(12, 8))

ax = fig.add_subplot(111)

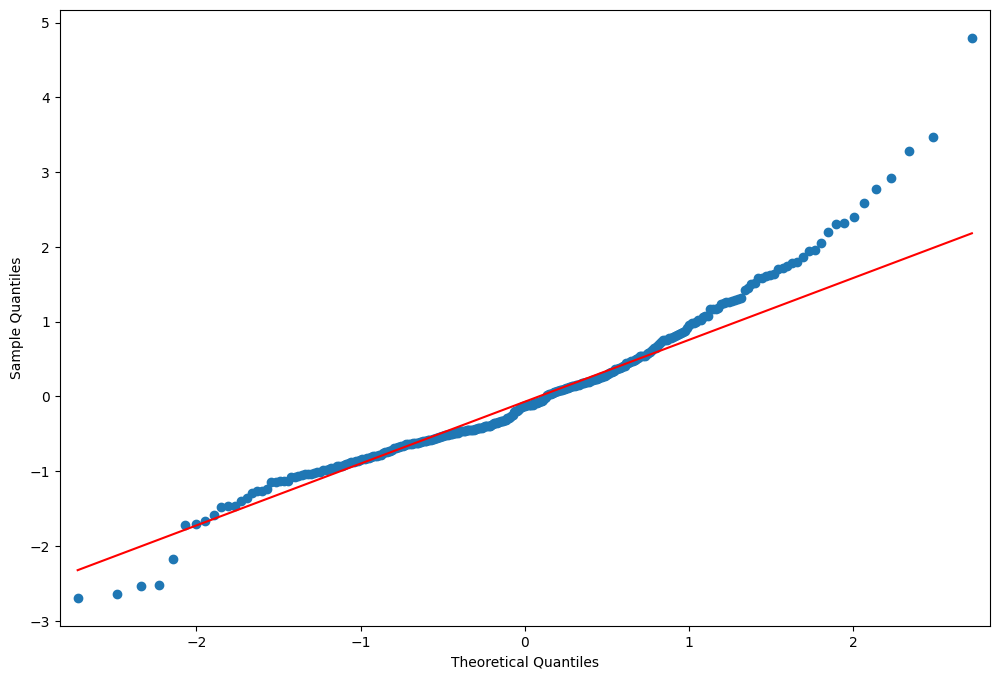

fig = qqplot(resid, line="q", ax=ax, fit=True)

[19]:

fig = plt.figure(figsize=(12, 8))

ax1 = fig.add_subplot(211)

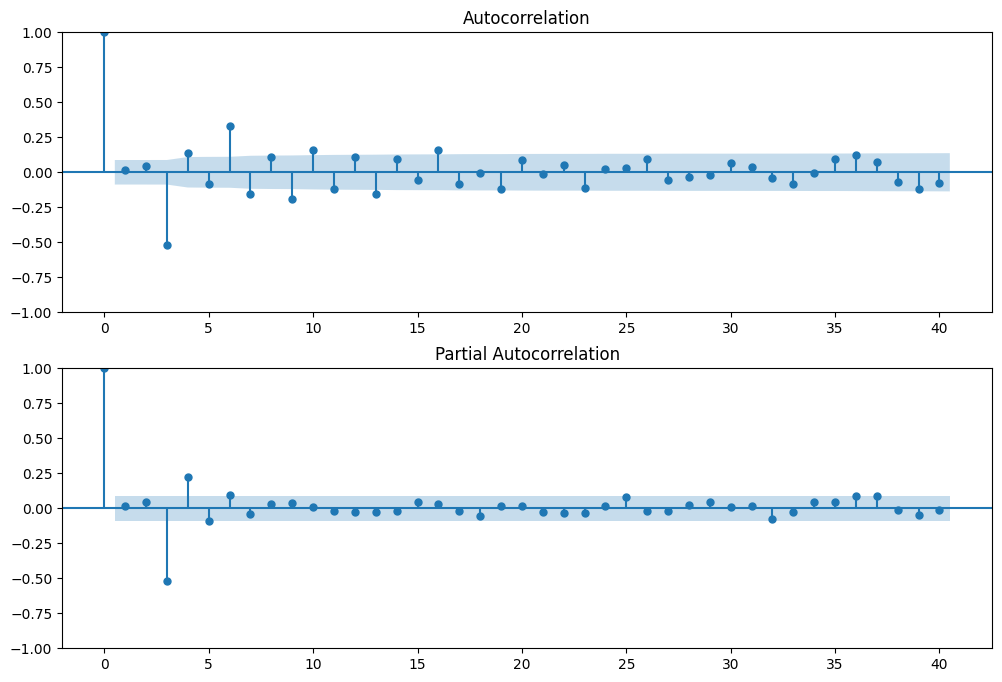

fig = sm.graphics.tsa.plot_acf(resid.values.squeeze(), lags=40, ax=ax1)

ax2 = fig.add_subplot(212)

fig = sm.graphics.tsa.plot_pacf(resid, lags=40, ax=ax2)

[20]:

r, q, p = sm.tsa.acf(resid.values.squeeze(), fft=True, qstat=True)

data = np.c_[np.arange(1, 25), r[1:], q, p]

[21]:

table = pd.DataFrame(data, columns=["lag", "AC", "Q", "Prob(>Q)"])

print(table.set_index("lag"))

AC Q Prob(>Q)

lag

1.0 0.009170 0.026239 8.713184e-01

2.0 0.041793 0.572982 7.508939e-01

3.0 -0.001338 0.573544 9.024612e-01

4.0 0.136086 6.408642 1.706385e-01

5.0 0.092465 9.111351 1.047043e-01

6.0 0.091947 11.792661 6.675737e-02

7.0 0.068747 13.296552 6.520425e-02

8.0 -0.015022 13.368601 9.978086e-02

9.0 0.187590 24.641072 3.394963e-03

10.0 0.213715 39.320758 2.230588e-05

11.0 0.201079 52.359565 2.346490e-07

12.0 0.117180 56.802479 8.580351e-08

13.0 -0.014057 56.866630 1.895209e-07

14.0 0.015398 56.943864 4.000370e-07

15.0 -0.024969 57.147642 7.746546e-07

16.0 0.080916 59.295052 6.876728e-07

17.0 0.041138 59.852008 1.111674e-06

18.0 -0.052022 60.745723 1.549418e-06

19.0 0.062496 62.040010 1.832778e-06

20.0 -0.010303 62.075305 3.383285e-06

21.0 0.074453 63.924941 3.195540e-06

22.0 0.124954 69.152954 8.984238e-07

23.0 0.093162 72.069214 5.803579e-07

24.0 -0.082152 74.344911 4.716006e-07

This indicates a lack of fit.

In-sample dynamic prediction. How good does our model do?

[22]:

predict_sunspots = arma_mod30.predict("1990", "2012", dynamic=True)

print(predict_sunspots)

1990-12-31 167.048337

1991-12-31 140.995022

1992-12-31 94.862115

1993-12-31 46.864439

1994-12-31 11.246106

1995-12-31 -4.718265

1996-12-31 -1.164628

1997-12-31 16.187246

1998-12-31 39.022948

1999-12-31 59.450799

2000-12-31 72.171269

2001-12-31 75.378329

2002-12-31 70.438480

2003-12-31 60.733987

2004-12-31 50.204383

2005-12-31 42.078584

2006-12-31 38.116648

2007-12-31 38.456730

2008-12-31 41.965644

2009-12-31 46.870948

2010-12-31 51.424878

2011-12-31 54.401403

2012-12-31 55.323515

Freq: YE-DEC, Name: predicted_mean, dtype: float64

[23]:

def mean_forecast_err(y, yhat):

return y.sub(yhat).mean()

[24]:

mean_forecast_err(dta.SUNACTIVITY, predict_sunspots)

[24]:

np.float64(5.634832966885551)

Exercise: Can you obtain a better fit for the Sunspots model? (Hint: sm.tsa.AR has a method select_order)¶

Simulated ARMA(4,1): Model Identification is Difficult¶

[25]:

from statsmodels.tsa.arima_process import ArmaProcess

[26]:

np.random.seed(1234)

# include zero-th lag

arparams = np.array([1, 0.75, -0.65, -0.55, 0.9])

maparams = np.array([1, 0.65])

Let’s make sure this model is estimable.

[27]:

arma_t = ArmaProcess(arparams, maparams)

[28]:

arma_t.isinvertible

[28]:

True

[29]:

arma_t.isstationary

[29]:

False

What does this mean?

[30]:

fig = plt.figure(figsize=(12, 8))

ax = fig.add_subplot(111)

ax.plot(arma_t.generate_sample(nsample=50))

[30]:

[<matplotlib.lines.Line2D at 0x7ff12d63a920>]

[31]:

arparams = np.array([1, 0.35, -0.15, 0.55, 0.1])

maparams = np.array([1, 0.65])

arma_t = ArmaProcess(arparams, maparams)

arma_t.isstationary

[31]:

True

[32]:

arma_rvs = arma_t.generate_sample(nsample=500, burnin=250, scale=2.5)

[33]:

fig = plt.figure(figsize=(12, 8))

ax1 = fig.add_subplot(211)

fig = sm.graphics.tsa.plot_acf(arma_rvs, lags=40, ax=ax1)

ax2 = fig.add_subplot(212)

fig = sm.graphics.tsa.plot_pacf(arma_rvs, lags=40, ax=ax2)

For mixed ARMA processes the Autocorrelation function is a mixture of exponentials and damped sine waves after (q-p) lags.

The partial autocorrelation function is a mixture of exponentials and dampened sine waves after (p-q) lags.

[34]:

lags = int(10 * np.log10(arma_rvs.shape[0]))

arma11 = ARIMA(arma_rvs, order=(1, 0, 1)).fit()

resid = arma11.resid

r, q, p = sm.tsa.acf(resid, nlags=lags, fft=True, qstat=True)

data = np.c_[range(1, lags + 1), r[1:], q, p]

table = pd.DataFrame(data, columns=["lag", "AC", "Q", "Prob(>Q)"])

print(table.set_index("lag"))

AC Q Prob(>Q)

lag

1.0 -0.001244 0.000778 9.777436e-01

2.0 0.052350 1.382049 5.010626e-01

3.0 -0.522181 139.090106 5.938063e-30

4.0 0.146506 149.951983 2.084573e-31

5.0 -0.091171 154.166872 1.731083e-31

6.0 0.337059 211.891306 5.568290e-43

7.0 -0.160920 225.075262 5.519054e-45

8.0 0.116132 231.955610 1.142179e-45

9.0 -0.195352 251.464207 4.895752e-49

10.0 0.166410 265.649428 2.760836e-51

11.0 -0.126465 273.858717 2.767679e-52

12.0 0.115015 280.662675 5.334651e-53

13.0 -0.159302 293.742050 4.899046e-55

14.0 0.095846 298.486519 2.444596e-55

15.0 -0.062853 300.531001 4.335557e-55

16.0 0.159244 313.681886 3.718133e-57

17.0 -0.089423 317.837389 2.317190e-57

18.0 0.002504 317.840655 1.018533e-56

19.0 -0.124735 325.959706 9.297882e-58

20.0 0.093960 330.576238 4.414194e-58

21.0 -0.016212 330.713971 1.708363e-57

22.0 0.054804 332.291098 3.279536e-57

23.0 -0.110592 338.726892 6.325402e-58

24.0 0.022742 338.999620 2.166837e-57

25.0 0.029459 339.458217 6.665490e-57

26.0 0.095294 344.266902 2.658405e-57

/opt/hostedtoolcache/Python/3.10.16/x64/lib/python3.10/site-packages/statsmodels/tsa/statespace/sarimax.py:966: UserWarning: Non-stationary starting autoregressive parameters found. Using zeros as starting parameters.

warn('Non-stationary starting autoregressive parameters'

/opt/hostedtoolcache/Python/3.10.16/x64/lib/python3.10/site-packages/statsmodels/tsa/statespace/sarimax.py:978: UserWarning: Non-invertible starting MA parameters found. Using zeros as starting parameters.

warn('Non-invertible starting MA parameters found.'

[35]:

arma41 = ARIMA(arma_rvs, order=(4, 0, 1)).fit()

resid = arma41.resid

r, q, p = sm.tsa.acf(resid, nlags=lags, fft=True, qstat=True)

data = np.c_[range(1, lags + 1), r[1:], q, p]

table = pd.DataFrame(data, columns=["lag", "AC", "Q", "Prob(>Q)"])

print(table.set_index("lag"))

AC Q Prob(>Q)

lag

1.0 -0.007899 0.031383 0.859389

2.0 0.004128 0.039972 0.980212

3.0 0.018095 0.205341 0.976722

4.0 -0.006766 0.228509 0.993949

5.0 0.018123 0.395044 0.995465

6.0 0.050690 1.700565 0.945078

7.0 0.010253 1.754087 0.972191

8.0 -0.011208 1.818176 0.986088

9.0 0.020292 2.028663 0.991006

10.0 0.001028 2.029204 0.996111

11.0 -0.014033 2.130285 0.997983

12.0 -0.023858 2.423052 0.998426

13.0 -0.002108 2.425342 0.999339

14.0 -0.018784 2.607562 0.999589

15.0 0.011317 2.673844 0.999805

16.0 0.042158 3.595554 0.999443

17.0 0.007943 3.628344 0.999734

18.0 -0.074312 6.504019 0.993685

19.0 -0.023378 6.789205 0.995255

20.0 0.002398 6.792213 0.997313

21.0 0.000488 6.792338 0.998515

22.0 0.017953 6.961578 0.999024

23.0 -0.038576 7.744617 0.998744

24.0 -0.029817 8.213410 0.998859

25.0 0.077850 11.415980 0.990674

26.0 0.040407 12.280577 0.989478

Exercise: How good of in-sample prediction can you do for another series, say, CPI¶

[36]:

macrodta = sm.datasets.macrodata.load_pandas().data

macrodta.index = pd.Index(sm.tsa.datetools.dates_from_range("1959Q1", "2009Q3"))

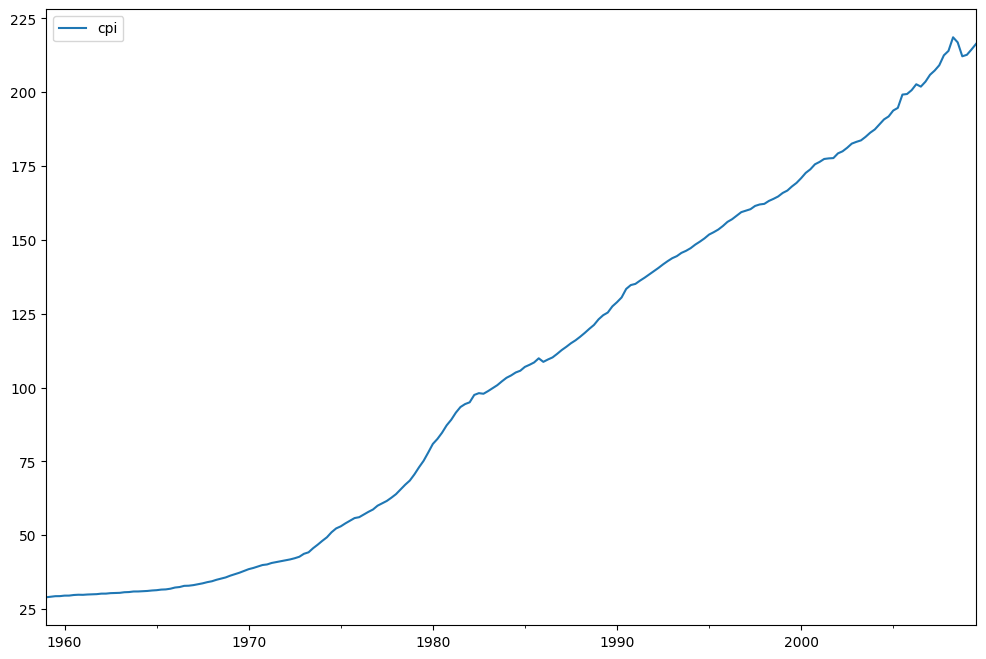

cpi = macrodta["cpi"]

Hint:¶

[37]:

fig = plt.figure(figsize=(12, 8))

ax = fig.add_subplot(111)

ax = cpi.plot(ax=ax)

ax.legend()

[37]:

<matplotlib.legend.Legend at 0x7ff12a3c67d0>

P-value of the unit-root test, resoundingly rejects the null of a unit-root.

[38]:

print(sm.tsa.adfuller(cpi)[1])

0.9904328188337422