VARMAX models¶

This is a brief introduction notebook to VARMAX models in statsmodels. The VARMAX model is generically specified as:

where \(y_t\) is a \(\text{k_endog} \times 1\) vector.

[1]:

%matplotlib inline

[2]:

import numpy as np

import pandas as pd

import statsmodels.api as sm

import matplotlib.pyplot as plt

[3]:

dta = sm.datasets.webuse('lutkepohl2', 'https://www.stata-press.com/data/r12/')

dta.index = dta.qtr

endog = dta.loc['1960-04-01':'1978-10-01', ['dln_inv', 'dln_inc', 'dln_consump']]

Model specification¶

The VARMAX class in statsmodels allows estimation of VAR, VMA, and VARMA models (through the order argument), optionally with a constant term (via the trend argument). Exogenous regressors may also be included (as usual in statsmodels, by the exog argument), and in this way a time trend may be added. Finally, the class allows measurement error (via the measurement_error argument) and allows specifying either a diagonal or unstructured innovation covariance matrix (via the

error_cov_type argument).

Example 1: VAR¶

Below is a simple VARX(2) model in two endogenous variables and an exogenous series, but no constant term. Notice that we needed to allow for more iterations than the default (which is maxiter=50) in order for the likelihood estimation to converge. This is not unusual in VAR models which have to estimate a large number of parameters, often on a relatively small number of time series: this model, for example, estimates 27 parameters off of 75 observations of 3 variables.

[4]:

exog = endog['dln_consump']

mod = sm.tsa.VARMAX(endog[['dln_inv', 'dln_inc']], order=(2,0), trend='n', exog=exog)

res = mod.fit(maxiter=1000, disp=False)

print(res.summary())

/home/travis/build/statsmodels/statsmodels/statsmodels/tsa/base/tsa_model.py:162: ValueWarning: No frequency information was provided, so inferred frequency QS-OCT will be used.

% freq, ValueWarning)

Statespace Model Results

==================================================================================

Dep. Variable: ['dln_inv', 'dln_inc'] No. Observations: 75

Model: VARX(2) Log Likelihood 361.036

Date: Fri, 21 Feb 2020 AIC -696.072

Time: 13:54:51 BIC -665.945

Sample: 04-01-1960 HQIC -684.043

- 10-01-1978

Covariance Type: opg

===================================================================================

Ljung-Box (Q): 61.20, 39.27 Jarque-Bera (JB): 11.47, 2.34

Prob(Q): 0.02, 0.50 Prob(JB): 0.00, 0.31

Heteroskedasticity (H): 0.45, 0.40 Skew: 0.16, -0.38

Prob(H) (two-sided): 0.05, 0.03 Kurtosis: 4.89, 3.43

Results for equation dln_inv

====================================================================================

coef std err z P>|z| [0.025 0.975]

------------------------------------------------------------------------------------

L1.dln_inv -0.2372 0.093 -2.544 0.011 -0.420 -0.054

L1.dln_inc 0.2837 0.449 0.632 0.528 -0.597 1.164

L2.dln_inv -0.1648 0.156 -1.057 0.290 -0.470 0.141

L2.dln_inc 0.0754 0.422 0.178 0.858 -0.752 0.903

beta.dln_consump 0.9544 0.640 1.492 0.136 -0.300 2.208

Results for equation dln_inc

====================================================================================

coef std err z P>|z| [0.025 0.975]

------------------------------------------------------------------------------------

L1.dln_inv 0.0636 0.036 1.782 0.075 -0.006 0.134

L1.dln_inc 0.0847 0.107 0.793 0.428 -0.125 0.294

L2.dln_inv 0.0098 0.033 0.298 0.765 -0.055 0.074

L2.dln_inc 0.0356 0.134 0.265 0.791 -0.227 0.299

beta.dln_consump 0.7684 0.112 6.853 0.000 0.549 0.988

Error covariance matrix

============================================================================================

coef std err z P>|z| [0.025 0.975]

--------------------------------------------------------------------------------------------

sqrt.var.dln_inv 0.0434 0.004 12.269 0.000 0.036 0.050

sqrt.cov.dln_inv.dln_inc 5.368e-05 0.002 0.027 0.979 -0.004 0.004

sqrt.var.dln_inc 0.0109 0.001 11.239 0.000 0.009 0.013

============================================================================================

Warnings:

[1] Covariance matrix calculated using the outer product of gradients (complex-step).

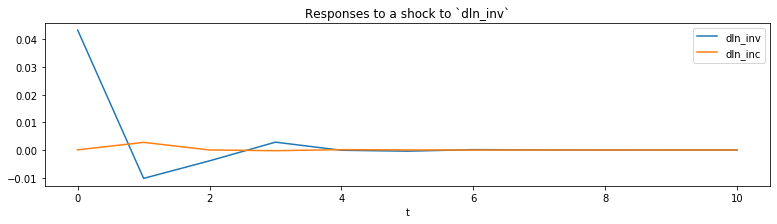

From the estimated VAR model, we can plot the impulse response functions of the endogenous variables.

[5]:

ax = res.impulse_responses(10, orthogonalized=True).plot(figsize=(13,3))

ax.set(xlabel='t', title='Responses to a shock to `dln_inv`');

Example 2: VMA¶

A vector moving average model can also be formulated. Below we show a VMA(2) on the same data, but where the innovations to the process are uncorrelated. In this example we leave out the exogenous regressor but now include the constant term.

[6]:

mod = sm.tsa.VARMAX(endog[['dln_inv', 'dln_inc']], order=(0,2), error_cov_type='diagonal')

res = mod.fit(maxiter=1000, disp=False)

print(res.summary())

/home/travis/build/statsmodels/statsmodels/statsmodels/tsa/base/tsa_model.py:162: ValueWarning: No frequency information was provided, so inferred frequency QS-OCT will be used.

% freq, ValueWarning)

Statespace Model Results

==================================================================================

Dep. Variable: ['dln_inv', 'dln_inc'] No. Observations: 75

Model: VMA(2) Log Likelihood 353.887

+ intercept AIC -683.774

Date: Fri, 21 Feb 2020 BIC -655.964

Time: 13:54:55 HQIC -672.670

Sample: 04-01-1960

- 10-01-1978

Covariance Type: opg

===================================================================================

Ljung-Box (Q): 68.83, 39.18 Jarque-Bera (JB): 12.37, 13.43

Prob(Q): 0.00, 0.51 Prob(JB): 0.00, 0.00

Heteroskedasticity (H): 0.44, 0.81 Skew: 0.05, -0.48

Prob(H) (two-sided): 0.04, 0.60 Kurtosis: 4.99, 4.84

Results for equation dln_inv

=================================================================================

coef std err z P>|z| [0.025 0.975]

---------------------------------------------------------------------------------

intercept 0.0182 0.005 3.803 0.000 0.009 0.028

L1.e(dln_inv) -0.2638 0.106 -2.499 0.012 -0.471 -0.057

L1.e(dln_inc) 0.5232 0.632 0.828 0.407 -0.715 1.761

L2.e(dln_inv) 0.0348 0.148 0.235 0.814 -0.255 0.324

L2.e(dln_inc) 0.1824 0.477 0.383 0.702 -0.752 1.117

Results for equation dln_inc

=================================================================================

coef std err z P>|z| [0.025 0.975]

---------------------------------------------------------------------------------

intercept 0.0207 0.002 13.029 0.000 0.018 0.024

L1.e(dln_inv) 0.0484 0.042 1.163 0.245 -0.033 0.130

L1.e(dln_inc) -0.0755 0.139 -0.542 0.588 -0.349 0.198

L2.e(dln_inv) 0.0177 0.042 0.419 0.676 -0.065 0.101

L2.e(dln_inc) 0.1298 0.153 0.849 0.396 -0.170 0.429

Error covariance matrix

==================================================================================

coef std err z P>|z| [0.025 0.975]

----------------------------------------------------------------------------------

sigma2.dln_inv 0.0020 0.000 7.366 0.000 0.001 0.003

sigma2.dln_inc 0.0001 2.33e-05 5.818 0.000 8.99e-05 0.000

==================================================================================

Warnings:

[1] Covariance matrix calculated using the outer product of gradients (complex-step).

Caution: VARMA(p,q) specifications¶

Although the model allows estimating VARMA(p,q) specifications, these models are not identified without additional restrictions on the representation matrices, which are not built-in. For this reason, it is recommended that the user proceed with error (and indeed a warning is issued when these models are specified). Nonetheless, they may in some circumstances provide useful information.

[7]:

mod = sm.tsa.VARMAX(endog[['dln_inv', 'dln_inc']], order=(1,1))

res = mod.fit(maxiter=1000, disp=False)

print(res.summary())

/home/travis/build/statsmodels/statsmodels/statsmodels/tsa/statespace/varmax.py:163: EstimationWarning: Estimation of VARMA(p,q) models is not generically robust, due especially to identification issues.

EstimationWarning)

/home/travis/build/statsmodels/statsmodels/statsmodels/tsa/base/tsa_model.py:162: ValueWarning: No frequency information was provided, so inferred frequency QS-OCT will be used.

% freq, ValueWarning)

Statespace Model Results

==================================================================================

Dep. Variable: ['dln_inv', 'dln_inc'] No. Observations: 75

Model: VARMA(1,1) Log Likelihood 354.288

+ intercept AIC -682.576

Date: Fri, 21 Feb 2020 BIC -652.449

Time: 13:54:57 HQIC -670.547

Sample: 04-01-1960

- 10-01-1978

Covariance Type: opg

===================================================================================

Ljung-Box (Q): 68.33, 39.15 Jarque-Bera (JB): 11.07, 14.06

Prob(Q): 0.00, 0.51 Prob(JB): 0.00, 0.00

Heteroskedasticity (H): 0.43, 0.91 Skew: 0.01, -0.46

Prob(H) (two-sided): 0.04, 0.81 Kurtosis: 4.88, 4.92

Results for equation dln_inv

=================================================================================

coef std err z P>|z| [0.025 0.975]

---------------------------------------------------------------------------------

intercept 0.0105 0.066 0.160 0.873 -0.118 0.139

L1.dln_inv -0.0061 0.699 -0.009 0.993 -1.375 1.363

L1.dln_inc 0.3822 2.763 0.138 0.890 -5.032 5.797

L1.e(dln_inv) -0.2484 0.709 -0.350 0.726 -1.638 1.141

L1.e(dln_inc) 0.1247 3.012 0.041 0.967 -5.779 6.029

Results for equation dln_inc

=================================================================================

coef std err z P>|z| [0.025 0.975]

---------------------------------------------------------------------------------

intercept 0.0165 0.027 0.601 0.548 -0.037 0.070

L1.dln_inv -0.0334 0.279 -0.119 0.905 -0.581 0.514

L1.dln_inc 0.2348 1.114 0.211 0.833 -1.950 2.419

L1.e(dln_inv) 0.0889 0.286 0.311 0.756 -0.471 0.649

L1.e(dln_inc) -0.2382 1.149 -0.207 0.836 -2.490 2.014

Error covariance matrix

============================================================================================

coef std err z P>|z| [0.025 0.975]

--------------------------------------------------------------------------------------------

sqrt.var.dln_inv 0.0449 0.003 14.523 0.000 0.039 0.051

sqrt.cov.dln_inv.dln_inc 0.0017 0.003 0.650 0.516 -0.003 0.007

sqrt.var.dln_inc 0.0116 0.001 11.712 0.000 0.010 0.013

============================================================================================

Warnings:

[1] Covariance matrix calculated using the outer product of gradients (complex-step).