Autoregressive Moving Average (ARMA): Sunspots data¶

[1]:

%matplotlib inline

[2]:

import numpy as np

from scipy import stats

import pandas as pd

import matplotlib.pyplot as plt

import statsmodels.api as sm

[3]:

from statsmodels.graphics.api import qqplot

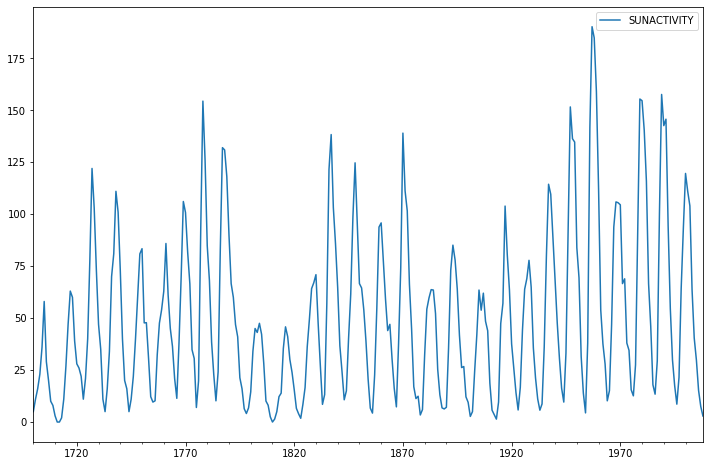

Sunspots Data¶

[4]:

print(sm.datasets.sunspots.NOTE)

::

Number of Observations - 309 (Annual 1700 - 2008)

Number of Variables - 1

Variable name definitions::

SUNACTIVITY - Number of sunspots for each year

The data file contains a 'YEAR' variable that is not returned by load.

[5]:

dta = sm.datasets.sunspots.load_pandas().data

[6]:

dta.index = pd.Index(sm.tsa.datetools.dates_from_range('1700', '2008'))

del dta["YEAR"]

[7]:

dta.plot(figsize=(12,8));

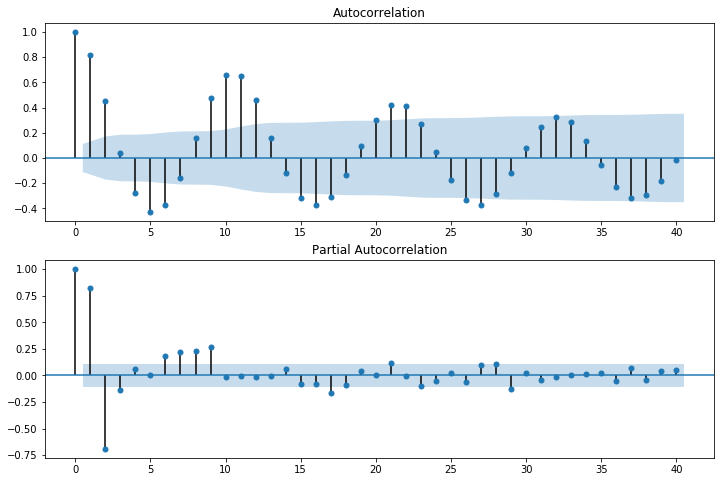

[8]:

fig = plt.figure(figsize=(12,8))

ax1 = fig.add_subplot(211)

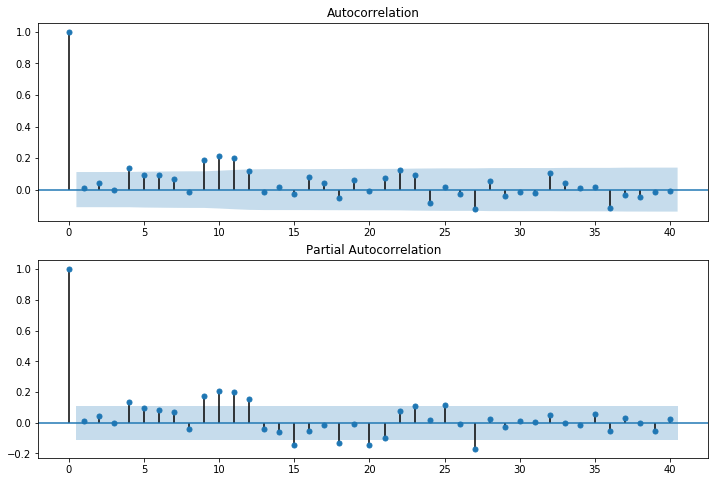

fig = sm.graphics.tsa.plot_acf(dta.values.squeeze(), lags=40, ax=ax1)

ax2 = fig.add_subplot(212)

fig = sm.graphics.tsa.plot_pacf(dta, lags=40, ax=ax2)

[9]:

arma_mod20 = sm.tsa.ARMA(dta, (2,0)).fit(disp=False)

print(arma_mod20.params)

const 49.659418

ar.L1.SUNACTIVITY 1.390656

ar.L2.SUNACTIVITY -0.688571

dtype: float64

/home/travis/build/statsmodels/statsmodels/statsmodels/tsa/base/tsa_model.py:162: ValueWarning: No frequency information was provided, so inferred frequency A-DEC will be used.

% freq, ValueWarning)

[10]:

arma_mod30 = sm.tsa.ARMA(dta, (3,0)).fit(disp=False)

/home/travis/build/statsmodels/statsmodels/statsmodels/tsa/base/tsa_model.py:162: ValueWarning: No frequency information was provided, so inferred frequency A-DEC will be used.

% freq, ValueWarning)

[11]:

print(arma_mod20.aic, arma_mod20.bic, arma_mod20.hqic)

2622.6363380637504 2637.569703171341 2628.6067259089964

[12]:

print(arma_mod30.params)

const 49.749905

ar.L1.SUNACTIVITY 1.300810

ar.L2.SUNACTIVITY -0.508093

ar.L3.SUNACTIVITY -0.129649

dtype: float64

[13]:

print(arma_mod30.aic, arma_mod30.bic, arma_mod30.hqic)

2619.4036286966934 2638.0703350811823 2626.866613503251

Does our model obey the theory?

[14]:

sm.stats.durbin_watson(arma_mod30.resid.values)

[14]:

1.9564806206172771

[15]:

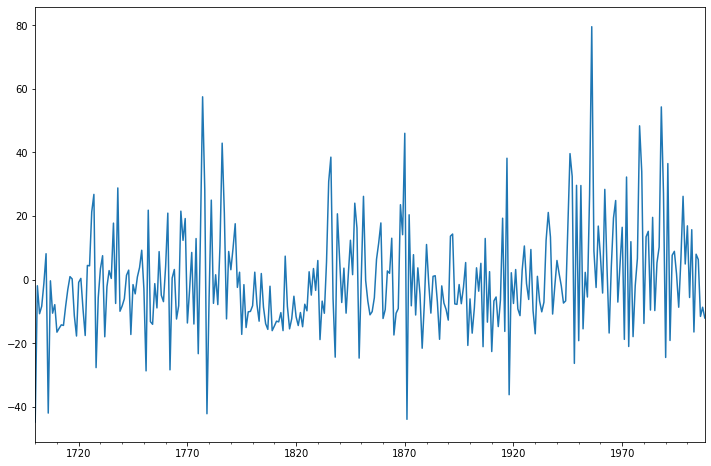

fig = plt.figure(figsize=(12,8))

ax = fig.add_subplot(111)

ax = arma_mod30.resid.plot(ax=ax);

[16]:

resid = arma_mod30.resid

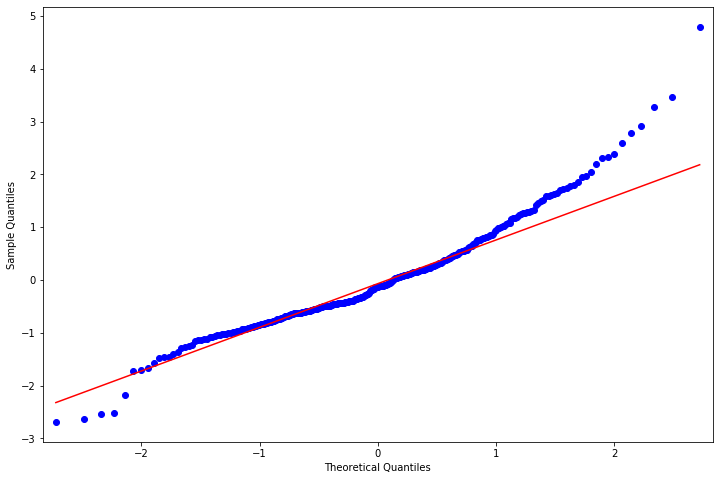

[17]:

stats.normaltest(resid)

[17]:

NormaltestResult(statistic=49.84504478123703, pvalue=1.5006729372147695e-11)

[18]:

fig = plt.figure(figsize=(12,8))

ax = fig.add_subplot(111)

fig = qqplot(resid, line='q', ax=ax, fit=True)

[19]:

fig = plt.figure(figsize=(12,8))

ax1 = fig.add_subplot(211)

fig = sm.graphics.tsa.plot_acf(resid.values.squeeze(), lags=40, ax=ax1)

ax2 = fig.add_subplot(212)

fig = sm.graphics.tsa.plot_pacf(resid, lags=40, ax=ax2)

[20]:

r,q,p = sm.tsa.acf(resid.values.squeeze(), fft=True, qstat=True)

data = np.c_[range(1,41), r[1:], q, p]

table = pd.DataFrame(data, columns=['lag', "AC", "Q", "Prob(>Q)"])

print(table.set_index('lag'))

AC Q Prob(>Q)

lag

1.0 0.009179 0.026287 8.712011e-01

2.0 0.041794 0.573049 7.508687e-01

3.0 -0.001335 0.573608 9.024467e-01

4.0 0.136089 6.408928 1.706198e-01

5.0 0.092468 9.111833 1.046858e-01

6.0 0.091948 11.793244 6.674345e-02

7.0 0.068748 13.297202 6.518981e-02

8.0 -0.015020 13.369229 9.976133e-02

9.0 0.187592 24.641919 3.393898e-03

10.0 0.213718 39.322016 2.229455e-05

11.0 0.201082 52.361172 2.344915e-07

12.0 0.117182 56.804233 8.574099e-08

13.0 -0.014055 56.868369 1.893868e-07

14.0 0.015398 56.945609 3.997587e-07

15.0 -0.024967 57.149364 7.741333e-07

16.0 0.080916 59.296810 6.872056e-07

17.0 0.041138 59.853777 1.110927e-06

18.0 -0.052021 60.747467 1.548409e-06

19.0 0.062496 62.041732 1.831616e-06

20.0 -0.010301 62.077019 3.381194e-06

21.0 0.074453 63.926697 3.193536e-06

22.0 0.124955 69.154818 8.978200e-07

23.0 0.093162 72.071085 5.799677e-07

24.0 -0.082152 74.346735 4.712934e-07

25.0 0.015695 74.430091 8.288901e-07

26.0 -0.025037 74.642950 1.367261e-06

27.0 -0.125861 80.041200 3.722497e-07

28.0 0.053225 81.010031 4.716196e-07

29.0 -0.038693 81.523858 6.916510e-07

30.0 -0.016904 81.622277 1.151641e-06

31.0 -0.019296 81.750988 1.868734e-06

32.0 0.104990 85.575117 8.927801e-07

33.0 0.040086 86.134619 1.247487e-06

34.0 0.008829 86.161863 2.047790e-06

35.0 0.014588 86.236500 3.263752e-06

36.0 -0.119329 91.248951 1.084435e-06

37.0 -0.036666 91.723920 1.521896e-06

38.0 -0.046193 92.480571 1.938700e-06

39.0 -0.017768 92.592941 2.990625e-06

40.0 -0.006220 92.606764 4.696901e-06

This indicates a lack of fit.

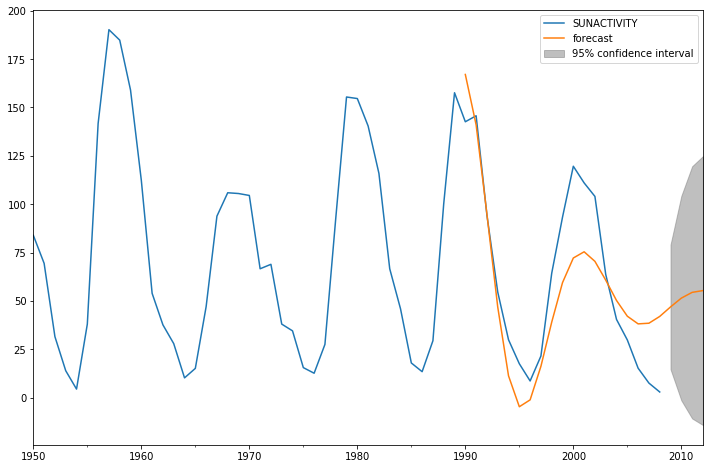

In-sample dynamic prediction. How good does our model do?

[21]:

predict_sunspots = arma_mod30.predict('1990', '2012', dynamic=True)

print(predict_sunspots)

1990-12-31 167.047383

1991-12-31 140.992929

1992-12-31 94.859019

1993-12-31 46.860813

1994-12-31 11.242529

1995-12-31 -4.721307

1996-12-31 -1.166890

1997-12-31 16.185729

1998-12-31 39.021913

1999-12-31 59.449874

2000-12-31 72.170109

2001-12-31 75.376718

2002-12-31 70.436375

2003-12-31 60.731501

2004-12-31 50.201726

2005-12-31 42.075980

2006-12-31 38.114265

2007-12-31 38.454638

2008-12-31 41.963816

2009-12-31 46.869281

2010-12-31 51.423242

2011-12-31 54.399683

2012-12-31 55.321642

Freq: A-DEC, dtype: float64

[22]:

fig, ax = plt.subplots(figsize=(12, 8))

ax = dta.loc['1950':].plot(ax=ax)

fig = arma_mod30.plot_predict('1990', '2012', dynamic=True, ax=ax, plot_insample=False)

[23]:

def mean_forecast_err(y, yhat):

return y.sub(yhat).mean()

[24]:

mean_forecast_err(dta.SUNACTIVITY, predict_sunspots)

[24]:

5.636993629037569

Exercise: Can you obtain a better fit for the Sunspots model? (Hint: sm.tsa.AR has a method select_order)¶

Simulated ARMA(4,1): Model Identification is Difficult¶

[25]:

from statsmodels.tsa.arima_process import ArmaProcess

[26]:

np.random.seed(1234)

# include zero-th lag

arparams = np.array([1, .75, -.65, -.55, .9])

maparams = np.array([1, .65])

Let’s make sure this model is estimable.

[27]:

arma_t = ArmaProcess(arparams, maparams)

[28]:

arma_t.isinvertible

[28]:

True

[29]:

arma_t.isstationary

[29]:

False

What does this mean?

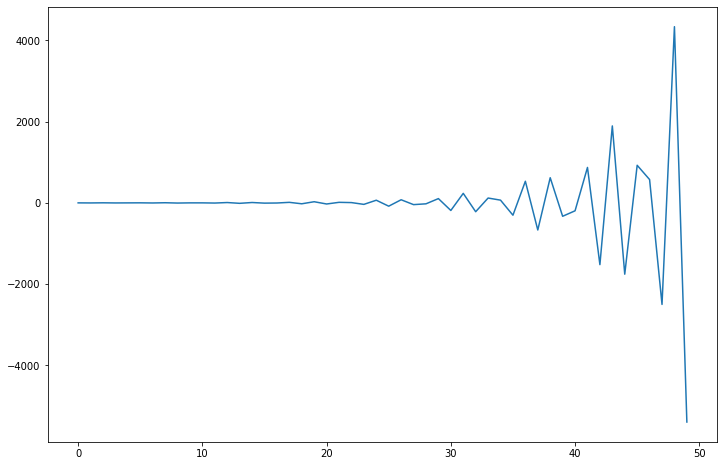

[30]:

fig = plt.figure(figsize=(12,8))

ax = fig.add_subplot(111)

ax.plot(arma_t.generate_sample(nsample=50));

[31]:

arparams = np.array([1, .35, -.15, .55, .1])

maparams = np.array([1, .65])

arma_t = ArmaProcess(arparams, maparams)

arma_t.isstationary

[31]:

True

[32]:

arma_rvs = arma_t.generate_sample(nsample=500, burnin=250, scale=2.5)

[33]:

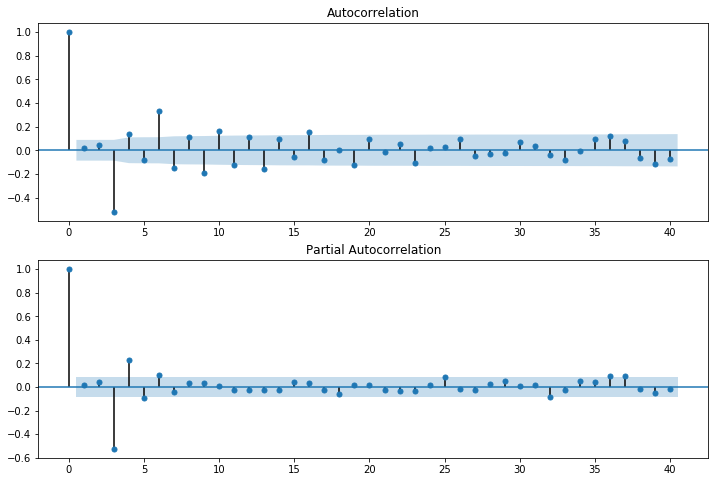

fig = plt.figure(figsize=(12,8))

ax1 = fig.add_subplot(211)

fig = sm.graphics.tsa.plot_acf(arma_rvs, lags=40, ax=ax1)

ax2 = fig.add_subplot(212)

fig = sm.graphics.tsa.plot_pacf(arma_rvs, lags=40, ax=ax2)

For mixed ARMA processes the Autocorrelation function is a mixture of exponentials and damped sine waves after (q-p) lags.

The partial autocorrelation function is a mixture of exponentials and dampened sine waves after (p-q) lags.

[34]:

arma11 = sm.tsa.ARMA(arma_rvs, (1,1)).fit(disp=False)

resid = arma11.resid

r,q,p = sm.tsa.acf(resid, fft=True, qstat=True)

data = np.c_[range(1,41), r[1:], q, p]

table = pd.DataFrame(data, columns=['lag', "AC", "Q", "Prob(>Q)"])

print(table.set_index('lag'))

AC Q Prob(>Q)

lag

1.0 0.254921 32.687679 1.082211e-08

2.0 -0.172416 47.670749 4.450700e-11

3.0 -0.420945 137.159394 1.548465e-29

4.0 -0.046875 138.271303 6.617697e-29

5.0 0.103240 143.675911 2.958716e-29

6.0 0.214864 167.133000 1.823717e-33

7.0 -0.000889 167.133402 1.009205e-32

8.0 -0.045418 168.185755 3.094832e-32

9.0 -0.061445 170.115804 5.837211e-32

10.0 0.034623 170.729856 1.958736e-31

11.0 0.006351 170.750557 8.267050e-31

12.0 -0.012882 170.835910 3.220231e-30

13.0 -0.053959 172.336547 6.181196e-30

14.0 -0.016606 172.478965 2.160215e-29

15.0 0.051742 173.864489 4.089542e-29

16.0 0.078917 177.094280 3.217937e-29

17.0 -0.001834 177.096028 1.093168e-28

18.0 -0.101604 182.471939 3.103820e-29

19.0 -0.057342 184.187772 4.624066e-29

20.0 0.026975 184.568285 1.235671e-28

21.0 0.062359 186.605964 1.530258e-28

22.0 -0.009400 186.652366 4.548192e-28

23.0 -0.068037 189.088184 4.562012e-28

24.0 -0.035566 189.755202 9.901092e-28

25.0 0.095679 194.592626 3.354283e-28

26.0 0.065650 196.874879 3.487619e-28

27.0 -0.018404 197.054614 9.008743e-28

28.0 -0.079244 200.394013 5.773702e-28

29.0 0.008499 200.432506 1.541383e-27

30.0 0.053372 201.953778 2.133189e-27

31.0 0.074816 204.949400 1.550158e-27

32.0 -0.071187 207.667250 1.262284e-27

33.0 -0.088145 211.843160 5.480804e-28

34.0 -0.025283 212.187455 1.215225e-27

35.0 0.125690 220.714908 8.231574e-29

36.0 0.142724 231.734123 1.923077e-30

37.0 0.095768 236.706168 5.937760e-31

38.0 -0.084744 240.607813 2.890873e-31

39.0 -0.150126 252.878989 3.962990e-33

40.0 -0.083767 256.707748 1.996165e-33

[35]:

arma41 = sm.tsa.ARMA(arma_rvs, (4,1)).fit(disp=False)

resid = arma41.resid

r,q,p = sm.tsa.acf(resid, fft=True, qstat=True)

data = np.c_[range(1,41), r[1:], q, p]

table = pd.DataFrame(data, columns=['lag', "AC", "Q", "Prob(>Q)"])

print(table.set_index('lag'))

AC Q Prob(>Q)

lag

1.0 -0.007888 0.031301 0.859571

2.0 0.004132 0.039906 0.980245

3.0 0.018103 0.205416 0.976710

4.0 -0.006760 0.228539 0.993948

5.0 0.018120 0.395025 0.995466

6.0 0.050688 1.700447 0.945087

7.0 0.010252 1.753954 0.972197

8.0 -0.011206 1.818017 0.986092

9.0 0.020292 2.028517 0.991009

10.0 0.001029 2.029059 0.996113

11.0 -0.014035 2.130167 0.997984

12.0 -0.023858 2.422925 0.998427

13.0 -0.002108 2.425215 0.999339

14.0 -0.018783 2.607428 0.999590

15.0 0.011316 2.673698 0.999805

16.0 0.042159 3.595418 0.999443

17.0 0.007943 3.628204 0.999734

18.0 -0.074311 6.503854 0.993686

19.0 -0.023379 6.789066 0.995256

20.0 0.002398 6.792072 0.997313

21.0 0.000487 6.792197 0.998516

22.0 0.017952 6.961434 0.999024

23.0 -0.038576 7.744465 0.998744

24.0 -0.029816 8.213248 0.998859

25.0 0.077850 11.415823 0.990675

26.0 0.040408 12.280447 0.989479

27.0 -0.018612 12.464274 0.992262

28.0 -0.014764 12.580185 0.994586

29.0 0.017650 12.746189 0.996111

30.0 -0.005486 12.762262 0.997504

31.0 0.058256 14.578543 0.994614

32.0 -0.040840 15.473082 0.993887

33.0 -0.019493 15.677307 0.995393

34.0 0.037269 16.425464 0.995214

35.0 0.086212 20.437447 0.976296

36.0 0.041271 21.358845 0.974774

37.0 0.078704 24.716877 0.938948

38.0 -0.029729 25.197054 0.944895

39.0 -0.078397 28.543385 0.891179

40.0 -0.014466 28.657576 0.909268

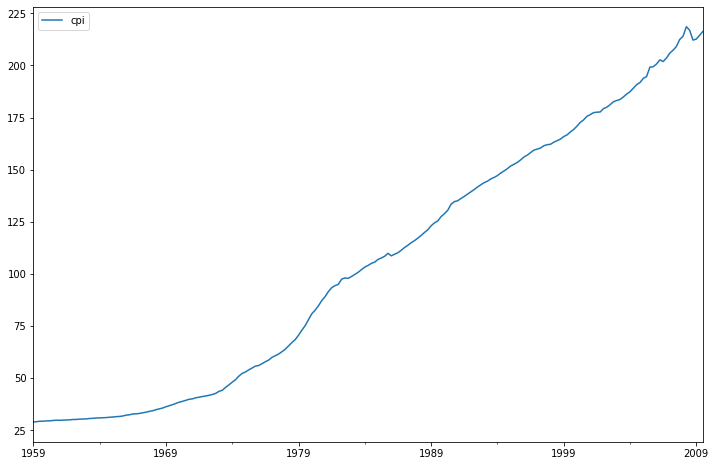

Exercise: How good of in-sample prediction can you do for another series, say, CPI¶

[36]:

macrodta = sm.datasets.macrodata.load_pandas().data

macrodta.index = pd.Index(sm.tsa.datetools.dates_from_range('1959Q1', '2009Q3'))

cpi = macrodta["cpi"]

Hint:¶

[37]:

fig = plt.figure(figsize=(12,8))

ax = fig.add_subplot(111)

ax = cpi.plot(ax=ax);

ax.legend();

P-value of the unit-root test, resoundingly rejects the null of a unit-root.

[38]:

print(sm.tsa.adfuller(cpi)[1])

0.9904328188337421